Aditya Vision

Aditya Vision

Bet on Consumer Appliances + Organised Retailing + Bharat's growth

Aditya Vision Limited (AVL), established in 1999, is a fast-growing electronic retail chain in East India. With 117 stores, across Bihar/Jharkhand, it has a clear focus on expanding reach in the Hindi heartland (50%+ market share in Bihar). They largely deal in Home Appliances (~70% of sales) like ACs, TVs, Fridges and Washing machines, while Digital gadgets & other electronics like mobile phones & speakers form ~30% of sales. Over FY18-23, it has increased its store count from 28 to 105, leading to revenue growth of 30%+. This has improved the overall scale of operation leading to more bargaining power, increasing its gross margins from a mere 9% to 16%. Consequently, profits have increased 25x in the last 5 years, and so has the stock price.

But is there still room for growth? Are the margins sustainable? Are the valuations stretched?

Electronic Retailing & Market Size

For a company to keep growing the market size & potential should be huge in respect of its current penetration:

Consumer Electronic is a huge market (~1 Lakh Cr) growing at 10-13%, with organised retailing growing at 12-15% due to a shift from the unorganized sector

Organised retail will keep gaining market share due to rising awareness, better pricing and additional value-added services (financing, customer care, etc.)

Penetration of consumer durables is one of the lowest in the Hindi Heartland (10%/14% penetration of Refrigerators in Bihar/ Jharkhand vs 38% penetration in India)

Staying in a Tier 3 city, I know that the buying potential of customers here is immense, as far as electronics are concerned.

Right-to-win for Organized Retail: While organized retail has a penetration of ~60% in this segment (vs 50% in FY16), we believe this penetration has room to grow to 70-80% over the next decade. For organised players, Gross Margins for Large Appliances & Phones are 16-20% and 6-10% respectively, giving a blended margin of ~12-13% for a store. National Players can leverage their scale to demand higher margins directly from the OEMs. For single-shop retailers, though, the gross margin is significantly less compared with regional or national players. This is because of lower bargaining power emanating from lower sales volume.

Threat of Online retailers: Penetration of online commerce in large electronics is lowest (~15%) vs other segments like Mobile (~60%), Laptops (~30%), Fashion (~27%) and Grocery (~16%). The penetration levels will be even lower in Tier 2/3 cities, where AVL stores are located. Tactile experience provides a unique advantage to physical stores, which online retail cannot match. In-store sales experience, installation and after-sales services are also the key value proposition.

What makes Aditya Vision different?

Best-in-class customer servicing: Leading to prioritised customer engagement, personalised service and trust (70% repeat customers)

Best Range, Lowest Price, Fast Installation (same day installation in the Hindi heartland where Flipkart/Amazon takes 5-15 days)

Great After Sales Service (extended warranty, financing, etc.)

Dedicated customer service no (Aditya Seva)

Well-trained staff (2 months training) with extreme customer obsession

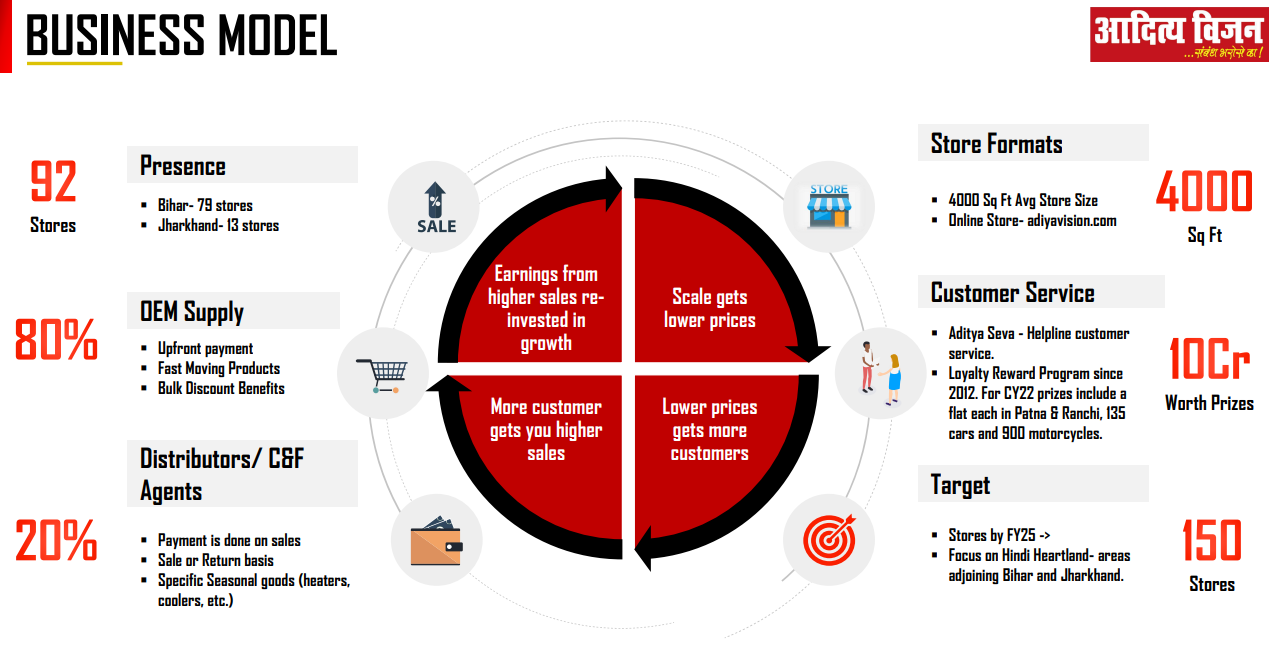

Sourcing: Direct relationship with OEMs accounts for ~80% of the sales, leading to bulk discount benefits.

Diversified product offerings comprising 10,000+ products ranging from digital gadgets to home appliances, all under one roof.

Efficient store operations: No stores closed in 24 years, stores are set up based on a “Creeping Cluster Approach” and strong market intelligence.

All, this has led to Adiya Vision enjoying 50%+ market share in its core market of Bihar, and it became the largest retailer in Jharkhand within 2-3 years of entry. Excellent sourcing relationship and scale have led to industry-leading gross margins of 15%+.

Management Overview

Business operations are managed by Mr Yashovardhan Sinha. The over two-decade-long experience of the promoter in the electronics retail industry, his strong understanding of market dynamics, healthy relationships with brand partners and ability to connect with the local population, have enabled a steady ramp up in scale of operations as reflected in the financials.

Management Remuneration (Directors & CFO) is ~5.6cr which seems reasonable and has remained the same for the last 2-3 years.

Promotors have sold ~6% of their holding over the last 1-2 years, but they still own a substantial 68% of the company.

Over the last year, the stock has garnered interest from FIIs, PMS Funds and large retail investors like Ashish Kacholi, thus has multiplied by 10-20x. This has also been because of the limited float of ~100-200cr available for retail investors (~90-95% is held by Promotors, PMSs and large retail investors)

The promotes also owns/manages one more listed retail company “Aditya Consumer”, which is into grocery retail and restaurants. It has ~95cr of sales and is valued at ~90cr. Going by the performance, it seems the promoters are not very invested in its day-to-day functioning. However, managing multiple companies can be seen as a risk.

Other than this, there doesn’t seem to be any other questionable related party transaction or corporate governance issue.

Store Unit Economics

A new store takes 6-8 months to break even and 3-4 years to pay back its entire capital. This strong unit economics is due to higher gross margins, low store rent and other expenses. The underlying thesis here is that compared to Metro, while the absolute gross margins from selling a TV/AC remain the same in a Tier 2 city, the absolute expenses are substantially lower.

It is a also huge operating leverage play, as once a new store is commissioned, the sales gradually increase from 6cr in Y1, 12cr in Y2 and 16cr in Y3. So the RoEs might look depressed initially as most of the cost like Rent, electricity, and inventory holding remains almost the same.

The management during its AGM confirmed that ~80% of sales in FY22 were from the 50% stores with 2.5yrs+ of operations (43 out of 79 stores). This exponential store addition has led to depressed sales per store and higher inventory days:

Customer’s Perspective

We tried comparing the prices across all the major online and offline retailers, from their websites. The offline & online prices can be different, but as per our channel checks, most of the retailers try to keep price parity between both channels.

Analysis of the data gave us the following insights:

While a customer knows beforehand which brands to purchase, the salesman can nudge them to consider a different brand, thus practically it’s the retailer who owns the customer.

Aditya Vision’s prices are ~3-4% premium to the lowest price retailers like Flipkart & Reliance Retail. But, the prices are still substantially lower than individual stores & smaller retail players

In absolute terms, the price difference was INR 1,000-1,500 (on a median basis). On negotiation, AVL’s staff will guarantee to match prices with Reliance and Croma.

Each OEM has a Minimum Operating Price (MOP), and all the retail companies need to abide by this informal slab. Thus, the scope for price competition is limited.

Basis the store reviews, Aditya Vision, Value Plus and Croma stand-out despite charging a premium versus other organised retail players

As per our store visits and online reviews, we can say that AVL’s focus has been towards customer satisfaction and service, which has built huge brand recall and trust among customers.

In most of the cities where AVL is present, it is only competing with regional retailers, where it has an advantage over price, staff, display, offers, service

Store aesthetics and display at AVL are at par with larger retailers like Reliance Digital and Vijay Sales. But AVL only focuses on 4 main products (TV, WM, Fridge, AC) thus providing better range and service to customers

AVL also gives away a lottery every year (1 coupon on every 10K purchases). This entails prizes worth 7-10cr each year.

AVL works on a cash-and-carry model with OEMs thus, they get 2-3% discounts on up-front payments, leading to higher margins.

Some of the store reviews:

Competition from Reliance Digital and Tata’s Croma:

Currently, these giants have stores only in Tier 2 cities like Patna, Gaya, Jamshedpur, Bhagalpur, Ranchi, Bokaro, Dhanbad

Both these retail giants have been focusing on increasing their presence in Tier 2/3 cities and have recently opened stores in smaller cities like Vijayapura, Vadodara, Solapur etc.

Croma aims to add 100+ stores each year, majorly in these smaller cities. Reliance Digital has 3,000+ stores, and further store additions will be in Tier 2/3 cities.

The key question will be, with rising competition is the premium pricing sustainable for the next 5-10 years? Will AVL be able to replicate its customer services & brand loyalty beyond its core states of Bihar?

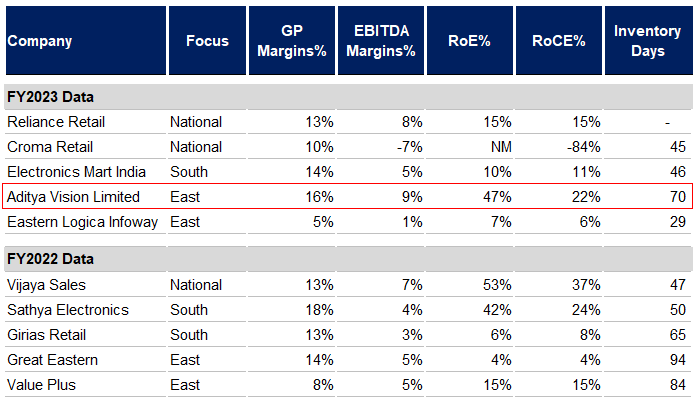

Competitor’s Benchmarking

We compared the financials and operations of all the major listed & unlisted electronic retailers:

Key Insights:

AVL has one of the highest gross margins, which is largely attributed to the premium pricing and better product mix. Digital gadgets & mobile phones (~8% gross margins) contribute ~15% of its sales vs 25-35% for Croma/Electronics Mart/Vijay Sales

Efficient store economics and higher margins translate to a superior RoCE and RoE for the company

Store Sales/sqft/day remain low at ~INR 98, compared to peer’s ~INR 115-125. This is depressed due to aggressive store expansion over the last 3 years. Similarly, inventory days are inflated at 70 days (vs ~40 days in FY18-20).

The avg. store size of AVL is 50% smaller compared to its peers, as most of the stores are located in Tier 2/3 cities.

Rental cost for AVL is lower than other retailers, as they are located more in Tier 2/3 cities and prefer opening stores in high streets rather than in malls.

AVL generates ~30-40% of revenues through the financing option (low compared to listed competitor, Electronic Mart, which generates 55%+ of its sales via financing). A store typically pays ~25% of the financing cost (subvention cost).

AVL’s Financials

ACL has shown an excellent track record of sales growth and margin improvement over the last decade:

AVL has compounded its sales at 24% over FY18-23, which is attributed towards Store addition @ 35% CAGR, ASP increase @ 9% CAGR, with a 14% decline in units sold per Sq.Ft:

Here are some of the store-level metrics for AVL:

Also, most of the RoE% improvement has been due to improvement in scale, which has led them to negotiate better rates from OEMs as now 80% of the sourcing is directly done from the brands.

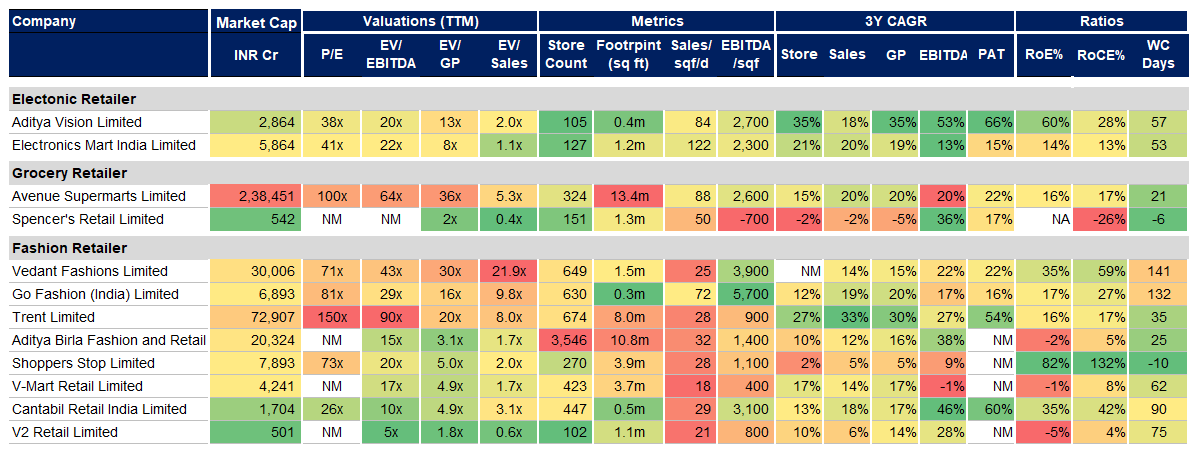

Valuations - Are all the +ves priced in?

Let’s look at the valuations of all the listed Retail companies in India:

The stock has run up quite a lot in the past 1-2 years and at the current price of INR 2,380 (Mkt Cap: 2,864 Cr.) it is trading at a high P/E ratio of ~38x.

While the company has shown a decent level of store addition and margin growth, we are unsure if this is sustainable. So, while projecting for the next 5 years, we have assumed a conservative level of growth and no significant margin expansion.

Despite a conservative projection and below-average exit multiple, we believe the stock can be a 2-3x bagger in the next 3 years.

Key risk: Aggressive store addition by Reliance Retail & Croma in Tier 2/3 cities; High entry valuations

Happy to hear your views on it. Reach out to me at p21ajit@iima.ac.in or +91 8982852903.

Disclaimer: I am not a SEBI-registered investment advisor. The information provided here is for education purposes only and is purely personal opinions. This report is neither an advice nor endorsement. Please do your own research and consult your financial advisor before making any decisions. I have a financial interest in the discussed security on the date of writing this report.